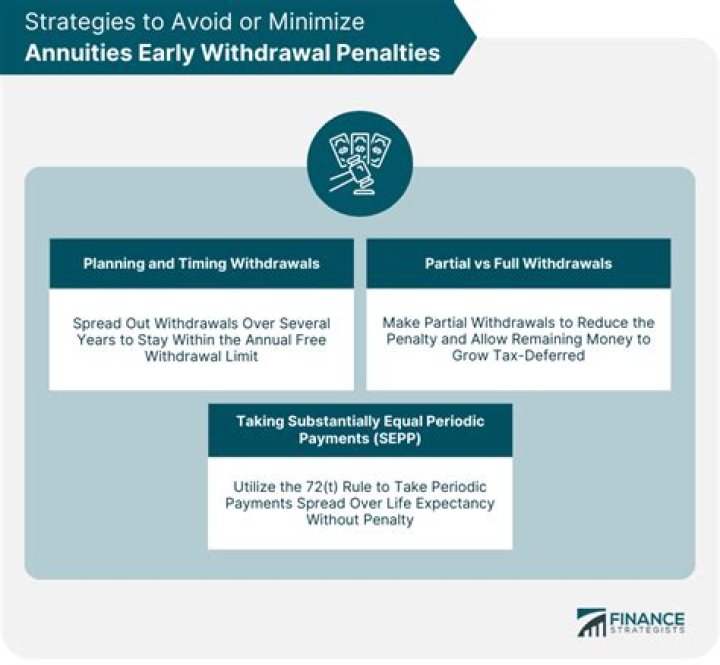

How do I offset early withdrawal penalty?

There are a few ways to reduce your the penalty on early IRA withdrawals, however.

- Emergency Withdrawals. The IRS offers penalty relief for certain unplanned withdrawals due to unexpected events, such as permanent disability or natural disaster.

- Discretionary Withdrawals.

- Rollover.

- SEPP.

- IRS Tax Forms.

How is early withdrawal penalty calculated?

To calculate the penalty on an early withdrawal, simply multiply the taxable distribution amount by 10%. An early distribution of $10,000, for example, would incur a $1,000 tax penalty, and it would be treated (and taxed) as additional income.

How to avoid the IRA early withdrawal penalty:

- Delay IRA withdrawals until age 59 1/2.

- Use the funds for large medical expenses.

- Purchase health insurance after a layoff.

- Pay for college costs.

- Fund part of a first home purchase.

- Defray birth or adoption costs.

- Manage disability expenses.

How to handle withdrawal symptoms when you decide to?

Here are some tips: 1 Plan more activities than you have time for. 2 Make a list of things to do when confronted with free time. 3 Move! Do not stay in the same place too long. 4 If you feel very bored when waiting for something or someone (a bus, your friend, your kids),… 5 Look at and listen to what is going on around you. 6 (more items)

How is the penalty for early withdrawal calculated?

Here’s an example to show how the early withdrawal penalty works. Suppose you are age 54 and you take $10,000 from your traditional IRA. The penalty would be calculated as follows: The $10,000 is considered income on your tax return.

When to take an early withdrawal from a retirement plan?

Here are a few key points to know about taking an early distribution: Early Withdrawals. An early withdrawal normally is taking cash out of a retirement plan before the taxpayer is 59½ years old. Additional Tax.

Do you have to pay taxes on a 10, 000 early withdrawal?

In addition to the tax on the $10,000 early withdrawal, a 10% penalty tax is assessed on the withdrawal. In this scenario, that would be an additional $1,000 of tax owed, in addition to the increase in your ordinary income taxes due to the additional $10,000 in income.