How do you correct cash basis in accounting?

How to convert cash basis to accrual basis accounting

- Add accrued expenses. Add back all expenses for which the company has received a benefit but has not yet paid the supplier or employee.

- Subtract cash payments.

- Add prepaid expenses.

- Add accounts receivable.

- Subtract cash receipts.

- Subtract customer prepayments.

Can I prepare my accounts on a cash basis?

You can record your income and expenses over the tax year either on a Cash Basis (i.e. when money actually enters and leaves your business, whether cash, card payment or cheque) or by using ‘traditional accounting’ methods (i.e. accruals basis – recording income and expenses when you invoice your customers or receive a …

Is there inventory in cash basis?

Inventory, including purchases and sales, must be treated on accrual-basis, but all other expenses and income may be considered under the cash method. If a business chooses to use the cash method for calculating income, however, then it must also use cash-basis for expenses.

Can a company prepare accounts on a cash basis?

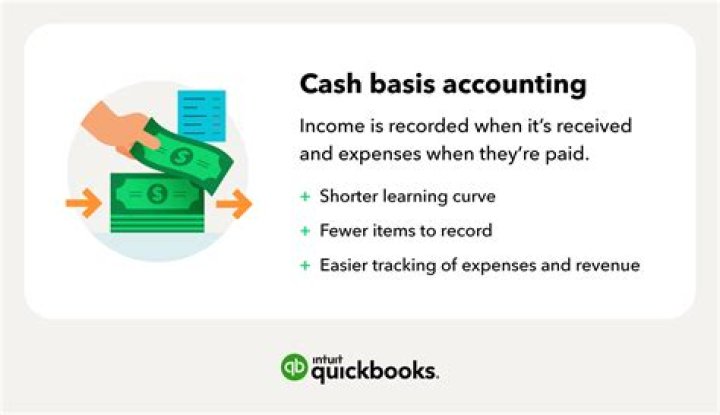

The cash basis of accounting allows certain businesses to work out their profit based on when money comes in and is paid out, rather than on when income is earned and costs incurred. Cash basis accounting is not available to all businesses, only to: sole traders. partnerships whose partners are all individuals.

What is the disadvantage of cash basis accounting?

One disadvantage of cash-basis accounting is that it gives your business a limited look at your income and expenses. Cash basis does not show your business’s liabilities. As a result, you may think you have more money to spend than you actually have.

Can you switch between cash and accrual?

If you want to change from using the accrual accounting method to cash basis accounting, you will ordinarily need to request permission to do so by filing Form 3115 with the IRS.

What is better cash basis or accrual basis?

Cash basis accounting is easier, but accrual accounting portrays a more accurate portrait of a company’s health by including accounts payable and accounts receivable. The accrual method is the most commonly used method, especially by publicly-traded companies as it smooths out earnings over time.

Why is accrual accounting better than cash basis?

Accrual accounting gives a better indication of business performance because it shows when income and expenses occurred. If you want to see if a particular month was profitable, accrual will tell you. Some businesses like to also use cash basis accounting for certain tax purposes, and to keep tabs on their cash flow.

When do you use cash basis in accounting?

Cash-basis accounting is a simple accounting method geared toward small business owners. If you run a small company, you may want to use the cash-basis method for your books. To use the cash-basis method, you record each transaction as money changes hands. When you pay a vendor, you record the expense.

Can a C corporation use the cash basis method?

Notably, prior to the Tax Cuts and Jobs Act, IRC Section 448 prevented C corporations with annual average gross receipts of $5 million or more for the three-prior-year taxable period from using the cash basis method. The Tax Cuts and Jobs Act, however, increased this amount to $25 million.

When to report Bas on cash or accruals basis?

We’ve noticed that business owners sometimes get confused when their BAS amount payable is considerably higher or lower than what they are expecting. Usually this happens when they report GST on a cash rather than an accruals, (or non-cash), basis.

When to switch from cash to accrual basis accounting?

Entities whose gross total receipts for the year is not more than $10,000,000 (In 2002, Revenue Procedure 2002-28 by the IRS extended the use of the cash method of accounting to certain qualifying small businesses with average annual revenues of between $1million and $10 million. in the previous year.)