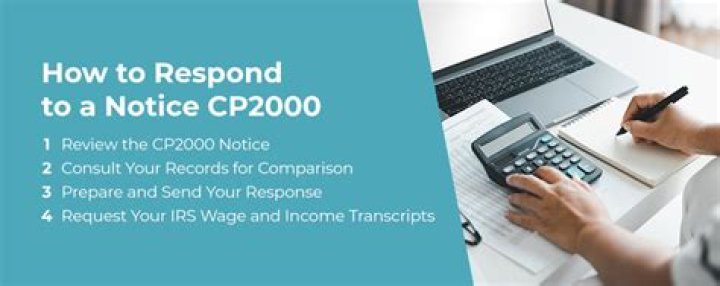

What do you need to know about the IRS Notice CP2000?

The IRS uses Notice CP2000 to inform you of proposed changes to your return based on information they have received from various third-party sources. Usually, the extra items are income, which increases your tax. Look carefully at the parts of the Notice CP2000 detailing the extra items that were missing from your return to see if you agree.

Do you need to amend your CP2000 return?

If the information displayed in the CP2000 notice is correct, you do not need to amend your return unless you have additional income, credits or expenses to report. If you agree with our notice, follow the instructions to sign and return the response form in the envelope provided or fax it to the number shown on the notice.

How long do you have to respond to a CP2000 notice?

You will usually have 30 days to respond to a CP2000 notice. If you need more time to find the documents you need, you can call the IRS to ask for more time. They will usually grant one 30-day extension if your original deadline hasn’t passed. An extension does not pause interest and penalties.

What’s the difference between notice cp2030 and notice cp2531?

Notice CP2030 is essentially the same in effect as Notice CP2531. Both indicate that the IRS has information that did not appear on the business tax return. This is not a bill and not an audit but is a math adjustment based on third party records. The IRS could audit you later.

What do you do with a CP2000 letter?

The videos explain the IRS Letters CP2000 and CP3219A and what to do with them. The videos also refer to additional resources at IRS.gov. The IRS Letter CP2000: Proposed Changes to Your Tax Return video tells taxpayers why they received this letter from the IRS and how to respond if they agree – or disagree – with the proposed changes.

What does the IRS letter cp3219a tell you?

The IRS Letter CP3219A: Statutory Notice of Deficiency video provides information about a proposed increase in tax and how the IRS figured this on the tax return. It also gives information about the taxpayer’s right to challenge the decision, if they choose to do so.