Are annuities affected by RMD?

Annuities held inside an IRA or 401(k) are subject to RMDs. Conversely, nonqualified annuities, funded with after-tax money, have no withdrawal requirement.

Does income annuity satisfy RMD?

A: Yes. Distributions made from qualified plans and/or IRAs count toward your annual RMD requirement. Divide the total amount you have invested in qualified plans and IRA accounts (except immediate annuities) by this divisor number. This will be your RMD withdrawal amount for this tax year.

Is income from annuities taxable?

Annuities are tax deferred. What this means is taxes are not due until you receive income payments from your annuity. Withdrawals and lump sum distributions from an annuity are taxed as ordinary income. They do not receive the benefit of being taxed as capital gains.

Do I need to take an RMD from my annuity?

Qualified variable annuities held in IRAs are subject to the IRS required minimum distribution (RMD) requirement. At age 72, qualified account owners are required to begin taking RMDs from their IRAs. Roth IRAs are not subject to RMDs while the account owner is alive.

When do you have to take the RMD on a variable annuity?

Qualified variable annuities held in IRAs are subject to the IRS required minimum distribution (RMD) requirement. At age 72, qualified account owners are required to begin taking the RMD from their IRAs. ROTH IRAs are not subject to the RMD while the account owner is alive. A 50% penalty on the RMD amount may be assessed if not taken as required.

How are RMDs calculated for a retirement account?

To calculate your RMDs for any given year you need two things: your total retirement account balances as of December 31 of that year, and the age you reach that year. Most retirees will use Table III below to determine what’s called the “distribution period”.

What’s the difference between a RMD and an IRA?

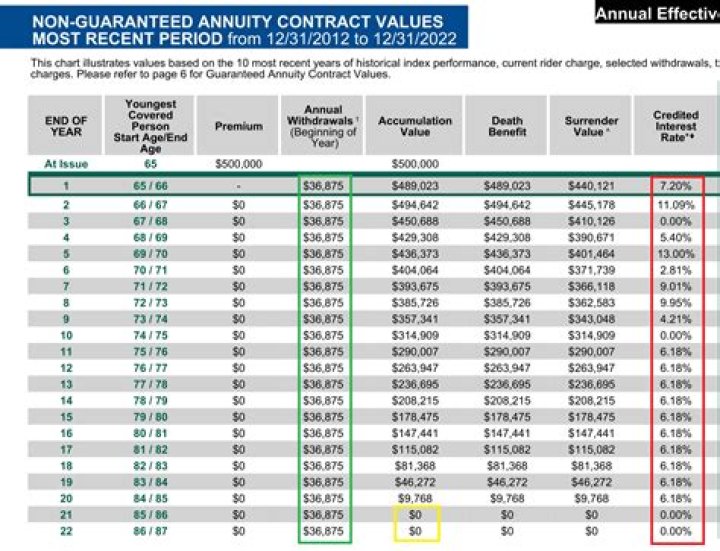

RMD distributions, on the other hand, are required to increase as a proportion of the total value of your IRA holdings as you age. So there is a unique challenge in fitting level immediate annuity payments into an increasing RMD model. Let’s look at an example to see why RMDs would not work for an immediate annuity.

What’s the minimum distribution for an immediate annuity?

So at age 70 the immediate annuity could be said to “over distribute” a larger share of your $100,000 than is required if you left the $100,000 in an IRA money market account. Now the annuity will continue to pay you $7,000 a year, equivalent to 7% of your initial premium, for the rest of your life.