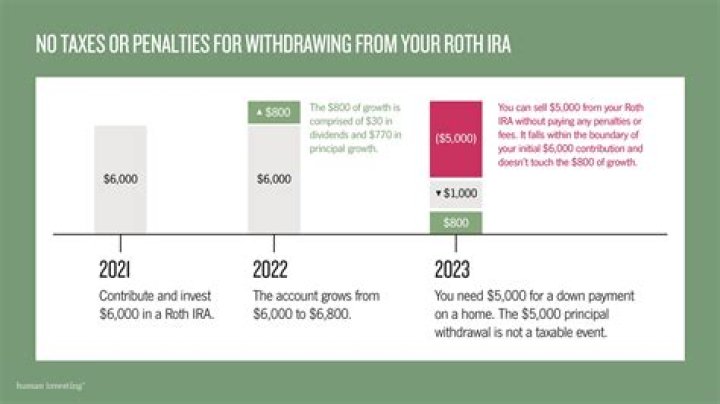

Can you withdraw your entire Roth IRA?

You can withdraw contributions you made to your Roth IRA anytime, tax- and penalty-free. However, you may have to pay taxes and penalties on earnings in your Roth IRA.

What is a non-qualified withdrawal from a Roth IRA?

A non-qualified distribution can refer to two scenarios: either a distribution from a Roth IRA that occurs before the IRA owner meets certain requirements or a distribution from an education savings account that exceeds the amount used for qualified education expenses.

What is a nonqualified distribution from a Roth IRA?

What happens if you take a non qualified withdrawal from a Roth IRA?

All other withdrawals from a Roth IRA that do not meet these criteria are considered non-qualified distributions. You’ll owe taxes and an early withdrawal penalty on any non-qualified funds you withdraw. The IRS treats withdrawals from a Roth IRA in a specific order.

Can you withdraw money from a Roth IRA at any time?

Because Roth IRA contributions are made with after-tax dollars, you can withdraw the contributions tax and penalty free at any time. That’s the simple part. But the beauty of a Roth is that the earnings can also be tax and penalty free.

How old do you have to be to make a qualified withdrawal from a Roth IRA?

Any earnings you withdraw are considered “qualified distributions” if you’re 59½ or older, and the account is at least five years old, making them tax- and penalty-free. Other kinds of withdrawals are considered “non-qualified” and can result in both taxes and penalties.

When do you get a qualified distribution from a Roth IRA?

A qualified distribution from your Roth IRA allows you to avoid taxes and the 10% early withdrawal penalty. To count as qualified, the distribution must meet both of these requirements: It occurs at least five years after you opened and funded your first Roth IRA (even if you’re withdrawing from a different one), and