How long does the underwriting process take on conventional loans?

According to Ellie Mae’s most recent data, conventional loans take an average of 51 days to close – 49 days on average for a purchase transaction and 51 days for a refinance. As we’ve mentioned, the underwriting part of this could take anywhere from a few days to a few weeks.

What do underwriters look for in a conventional loan?

When trying to determine whether you have the means to pay off the loan, the underwriter will review your employment, income, debt and assets. They’ll look at your savings, checking, 401k and IRA accounts, tax returns and other records of income, as well as your debt-to-income ratio.

Do conventional loans get denied in underwriting?

Even if you are pre-approved, your underwriting can still be denied. Your loan is never fully approved until the underwriter confirms that you are able to pay back the loan. Underwriters can deny your loan application for several reasons, from minor to major.

Why would an underwriter deny a conventional loan?

Whether in the beginning or end, reasons for a mortgage loan denial may include credit score drop, property issues, fraud, job loss or change, undisclosed debt, and more.

How long does underwriting take? Underwriting—the process by which mortgage lenders verify your assets, and check your credit scores and tax returns before you get a home loan—can take as little as two to three days. Typically, though, it takes over a week for a loan officer or lender to complete.

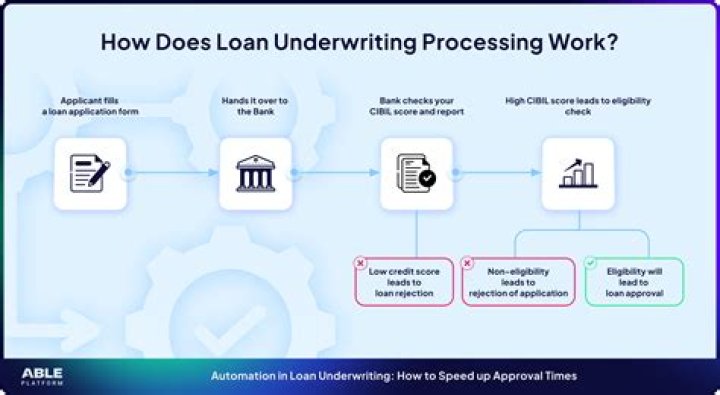

What are the steps in the underwriting process?

Here are the steps in the mortgage underwriting process and what you can expect. Step 1: Complete your mortgage application. The first step is to fill out a loan application. The information you provide will help determine if you’re eligible for a loan.

What does underwriting mean for a home loan?

You may have heard the term before, but what does underwriting mean exactly? Mortgage underwriting is what happens behind the scenes once you submit your application. It’s the process a lender uses to take an in-depth look at your credit and financial background to determine if you’re eligible for a loan.

What do I need to submit for mortgage underwriting?

When you submit a mortgage application to a lender, you’ll need to include extensive financial documentation, such as W-2 forms, pay stubs, bank statements and tax returns. When underwriting the application, the lender might come back to you with questions about these documents or requests for additional information.

How long does it take for a loan to go through underwriting?

How long does underwriting take? Mortgage lenders have different ‘turn times’ — the time it takes from your loan being submitted for underwriting review to the final decision. The full mortgage loan process often takes between 30 and 45 days from underwriting to closing. But turn times can be impacted by a number of different factors, like: