What does it mean to capitalize interest on investment?

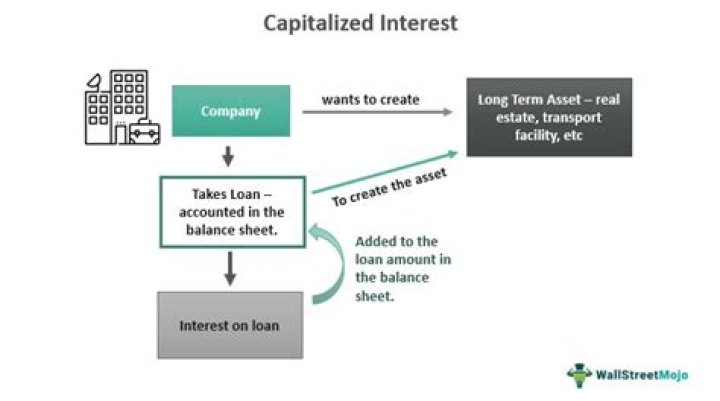

Capitalized interest is interest that is added to the total cost of a long-term asset or loan balance. This makes it so the interest is not recognized in the current period as an interest expense. Capitalized interest appears on the balance sheet rather than the income statement.

Is interest on construction loan tax deductible?

This is an itemized personal deduction you take on IRS Schedule A. So long as the home becomes your main home or second home on the day it’s ready for occupancy, you can deduct all the interest you paid on the construction loan within 24 months before the home was completed.

How do you calculate monthly interest on a construction loan?

Let’s say the interest rate on your construction loan is 6%. The 6% is an annual number, and 6 divided by 12 is 0.5, so your monthly interest rate is 0.5%. You’ve borrowed $50,000 so far, so 0.5% of that is $250. That’s going to be your interest payment next month.

How is interest capitalized in the construction of an asset?

Capitalized interest is the cost of the funds used to finance the construction of a long-term asset that an entity constructs for itself. The capitalization of interest is required under the accrual basis of accounting, and results in an increase in the total amount of fixed assets appearing on the balance sheet. Click to see full answer

What kind of costs are capitalized during construction?

What costs are capitalized during construction? Capitalized costs typically arise in relation to the construction of buildings, where most construction costs and related interest costs can be capitalized. Examples of capitalized costs include: Materials used to construct an asset. Sales taxes related to assets purchased for use in a fixed asset.

Why is capitalized interest included in historical cost?

To set the acquiring assets up for their intended use for a period of time, capitalized interest is part of the historical cost.

When do I need to capitalize my interest?

§ 1.263A-8 Requirement to capitalize interest. (1)General rule. Capitalization of interest under the avoided cost method described in § 1.263A-9 is required with respect to the production of designated property described in paragraph (b) of this section. (2)Treatment of interest required to be capitalized.