Can a multi-member LLC be disregarded?

The short answer is no, a Multi-Member LLC is rarely a Disregarded Entity. By default, a Multi-Member LLC will be taxed as a Partnership. If the Multi-Member LLC wants to be taxed as a Corporation instead, it needs to make a special election with the IRS.

How is multi member LLC taxed?

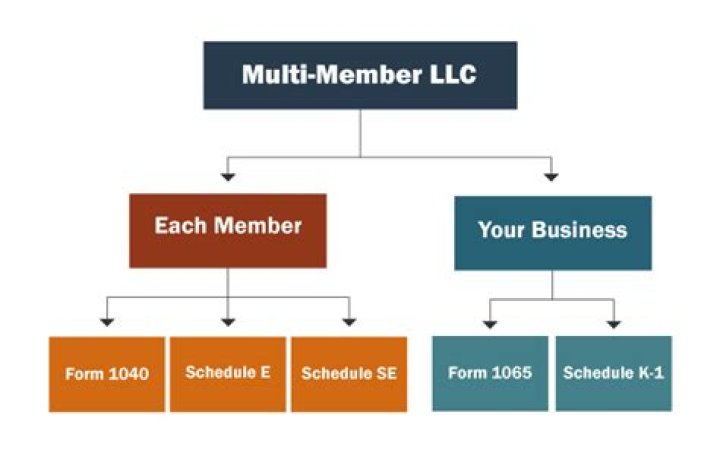

Multi-member LLCs are taxed as partnerships and do not file or pay taxes as the LLC. Instead, the profits and losses are the responsibility of each member; they will pay taxes on their share of the profits and losses by filling out Schedule E (Form 1040) and attaching it to their personal tax return.

What is a single-member LLC that is disregarded?

A disregarded entity refers to a business entity with one owner that is not recognized for tax purposes as an entity separate from its owner. A single-member LLC ( “SMLLC”), for example, is considered to be a disregarded entity. As the result of being “disregarded,” the SMLLC does not file a separate tax return.

How do I make my LLC a disregarded entity?

In order for a business to be considered a disregarded entity, two things must be true:

- The business structure must be separate from the owner in terms of liability.

- The business must be taxed through the owner’s personal tax return using Schedule C to determine the net income.

How do you know if your LLC is a disregarded entity?

If a single-member LLC does not elect to be treated as a corporation, the LLC is a “disregarded entity,” and the LLC’s activities should be reflected on its owner’s federal tax return.

How is a disregarded entity different from a single member LLC?

Like single-member LLCs, corporations are separate entities created by their owners for a specific purpose. Unlike single-member LLCs, corporations are taxed separately for the most part. A sole proprietorship is not a disregarded entity because it isn’t a separate entity.

When to transfer membership interest in a LLC?

When a member of your LLC wishes to transfer the entirety of his or her membership interest to another person or entity, you have to create a document called Membership Interest Assignment. This document is usually used when a member is leaving the company or wants to entirely relinquish his or her interest.

When to change a disregarded entity to a corporation?

Single-member LLCs can choose to change its tax designation to a corporation at any time. This step can be appropriate if the business has grown larger. However, it comes with additional tax complications. Single-member LLCs can also become partnerships if another partner joins the company. In both cases, the LLC is no longer a disregarded entity.

Can a disregarded entity switch to the first method?

An owner of multiple disregarded entities can choose the first method for some of those entities and the second method for others. Further, an owner may switch from the second method to the first method for a succeeding taxable year. However, IRS consent is required to switch from the first method to the second.